The Endowment

Related Links

Investment Performance

The University of Chicago’s endowment finished fiscal year 2012 with a market value of $6.57 billion, including $870 million of Medical Center endowment. This includes $277 million generated from investment returns during fiscal year 2012. Ninety-three percent of the endowment is invested in the Total Return Investment Pool (TRIP). TRIP’s return, net of outside management fees, was +6.8 percent for the fiscal year. For the three years ended June 30, 2012, TRIP’s return ranked first of the 20 largest private endowments; TRIP’s return ranked second for the five-year period (see figure 1).

The strong recovery of the endowment after the global financial crisis of 2008 and 2009 has taken place even as the University established a lower risk profile and significantly improved liquidity. The three-year results reflect positive returns from equities, private markets, and bonds, together with strong performance by the University’s investment managers.

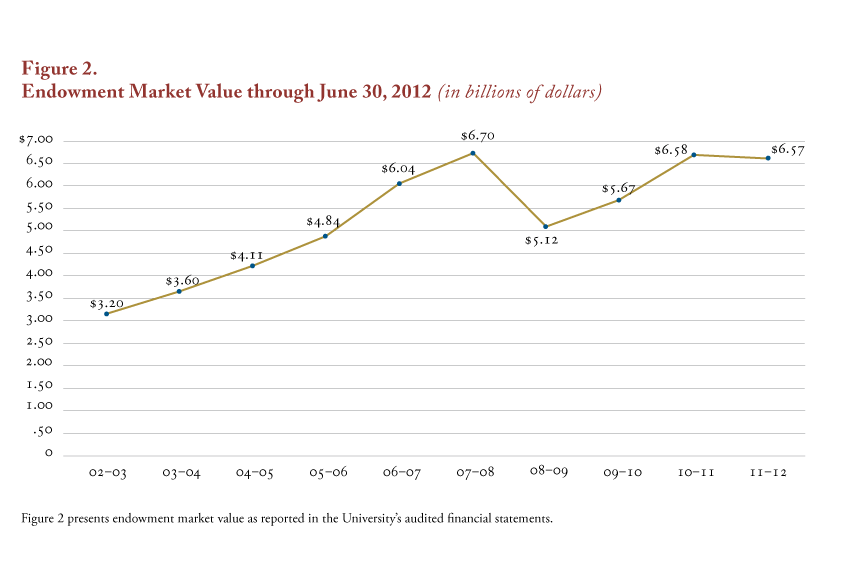

The endowment’s long-term performance is especially important given its dual role of providing support for current operations and for future generations. Between June 30, 2003, and June 30, 2012, with the help of solid investment returns, generous alumni support, and prudent spending, the endowment increased from $3.20 billion to $6.57 billion (see figure 2). During that period, the University earned an average annual return of 9.6 percent or 148 basis points ahead of the benchmark, while gifts to endowment totaled $776 million.

Endowment Management and Asset Allocation

The Investment Committee of the Board of Trustees is responsible for overseeing the investment of endowment funds. The committee’s all-volunteer members, most of whom have significant professional experience managing investments, are trustees of the University. The mission of the University of Chicago’s Office of Investments and the Investment Committee of the Board of Trustees is to provide stewardship of the University’s investment assets. This includes managing the University’s endowment to support the University’s academic programs and ensure that the endowment benefits both current and future generations. The University’s endowment is largely invested in the Total Return Investment Pool (TRIP).

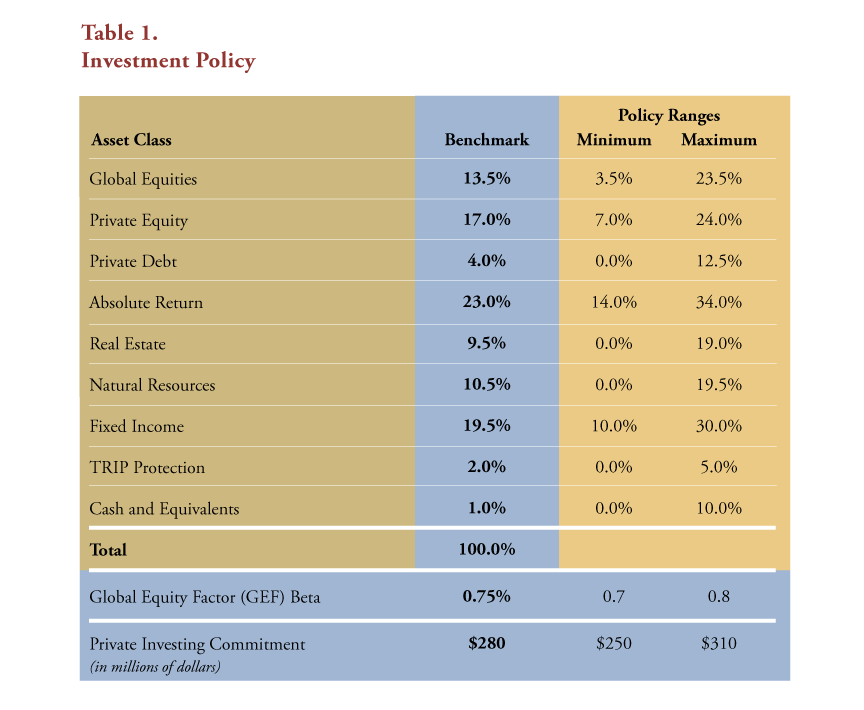

The investment objective of TRIP is to achieve a high return consistent with a level of risk that is appropriate for the University. The Investment Office takes a Total Enterprise Asset Management (TEAM) approach in designing the investment strategy of TRIP. A TEAM approach takes into account the economic risks borne by the University, such as growth objectives and debt ratios, in selecting an appropriate level of risk for TRIP. Our primary measure of risk in the portfolio is the Global Equity Factor (GEF), a metric that is similar in concept to beta. A secondary measure of risk in the portfolio is the amount of private investments that should be targeted.

Through the TEAM approach, the Investment Office, in consultation with the Investment Committee, has determined that a portfolio with a central tendency GEF of 0.75 is appropriate for the University. TRIP’s GEF is allowed to vary between 0.7 and 0.8 (see table 1). Furthermore, the portfolio seeks to achieve exposure to private assets of approximately 35 percent over time, in normal market environments. The portfolio is currently above its intended private investment target and is expected to meet this target within the next three years, due to a natural evolution of the life cycle of private investing. Going forward, the exposure to private assets may vary widely depending on market conditions. Should there be material changes to the financial conditions of the University or investment markets, the Investment Office and Investment Committee may revisit these parameters.

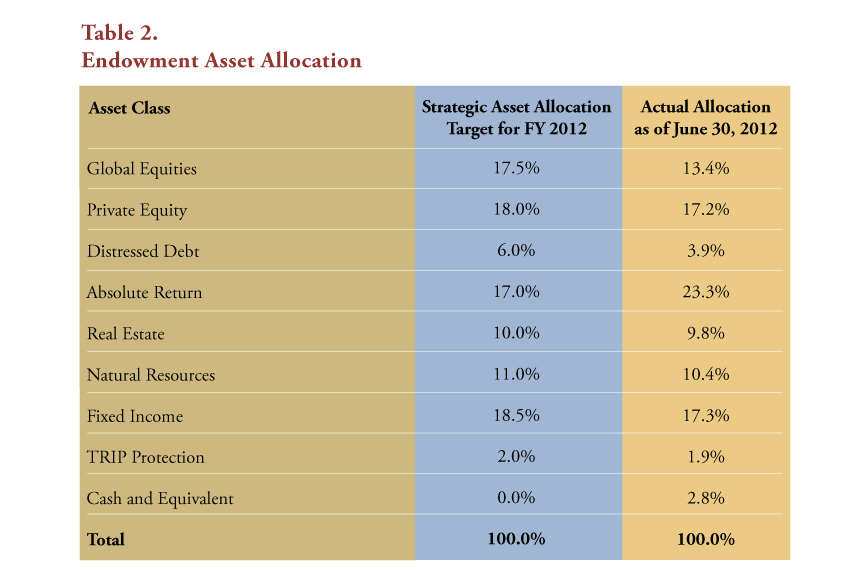

TRIP invests in a broad array of assets, including global stocks and bonds, real estate, natural resources, private equities, absolute return strategies, and protection (tail hedging strategies) (see table 2). The Investment Office achieves exposure to these categories by selecting and engaging external managers. The Investment Office may also make direct investments and co-investments in these asset categories, and use listed derivatives to ensure adherence to investment policy and risk parameters. In seeking to maximize returns given these risk parameters, the Investment Office recommends an annual investment plan of broad asset class ranges and a private investment commitment budget, which is reviewed and approved by the Investment Committee. The annual investment plan is meant to be an implementable policy statement of our TEAM-driven risk and liquidity targets, rather than superseding these targets.

The Role of the Endowment

The fundamental purpose of the University’s endowed funds is to support the core academic mission of the University by supplying a steady source of income to supplement the operating budget. Currently, the endowment provides 12 percent of total revenue.

Spending from the endowment is used primarily for academic purposes, going toward academic programs, instruction and research, faculty salary support, student aid, library acquisitions, and maintenance of the buildings and classrooms.

Maintaining and growing the value of the endowment over time is critical to ensuring that the steady source of income the endowment provides will not be eroded. At the University of Chicago, that is accomplished in a number of ways, including a well-diversified portfolio and a conservative spending policy.

Endowment Spending

The control of endowment spending, a critical factor in maintaining value over time, is a responsibility that is vested in the trustees of the University. Each year as part of the budget process, the trustees are asked to approve a level of spending that is within the range of 4.5 to 5.5 percent of a 12-quarter average market value, lagged one year. The flexibility afforded the trustees by virtue of the range allows them to lower the rate of spending during periods of market appreciation and to increase it during periods of decline. This spending rule, which was implemented with the fiscal year 2005, is designed to strike a healthy balance between long-term asset preservation and prudent spending for current operations. It has the added benefit of cushioning the payout from sudden swings or shocks in the financial markets.